Every year the same financial emergencies happen to the same people.

The car registration bill arrives and there is no money set aside. The annual insurance premium hits and it goes on a credit card. The holiday season rolls around and December becomes a month of financial recovery rather than celebration. The laptop breaks and an emergency fund that was supposed to cover real emergencies gets drained by something entirely predictable.

None of these are emergencies. They are known future expenses that were never planned for.

A sinking fund fixes this permanently — and it is one of the simplest, most effective personal finance tools that almost nobody uses correctly.

What Is a Sinking Fund

A sinking fund is money you set aside gradually over time for a specific planned future expense.

The name comes from accounting — businesses have used sinking funds for centuries to set aside money incrementally for large future obligations like debt repayment or equipment replacement. The personal finance version works on exactly the same principle.

Instead of scrambling to find $1,200 when your car insurance is due, you set aside $100 every month for 12 months. When the bill arrives the money is already there. No credit card. No emergency fund drain. No financial stress.

The mechanics are simple:

Target Amount ÷ Months Until Due = Monthly ContributionThat is the entire calculation. The power is not in the math — it is in the habit of treating future expenses as present responsibilities.

The Difference Between a Sinking Fund and an Emergency Fund

These two tools are frequently confused — and using them interchangeably destroys the effectiveness of both.

| Sinking Fund | Emergency Fund | |

|---|---|---|

| Purpose | Known future expenses | Unknown unexpected expenses |

| Examples | Car insurance, vacation, holiday gifts | Job loss, medical emergency, major repair |

| Timeline | Specific target date | No target date — always available |

| Amount | Exact target amount | 3-6 months of living expenses |

| Predictability | Fully predictable | Completely unpredictable |

Your emergency fund should only be touched for genuine emergencies — unexpected events that could not have been planned for. Car registration is not an emergency. It happens every year on the same date. Draining your emergency fund for predictable expenses leaves you genuinely exposed when something unexpected actually happens.

Sinking funds protect your emergency fund by handling everything predictable — so your emergency fund only ever faces actual emergencies.

Why Most People Never Set Up Sinking Funds

The concept is simple enough that most people nod along when they hear about it and then never implement it. Three reasons explain why:

It requires thinking months ahead. Most budgeting focuses on this month — income, expenses, savings. Sinking funds require you to look 3, 6, or 12 months into the future and allocate money today for something you will not pay until later. That mental shift is uncomfortable for people living paycheck to paycheck.

The money feels unproductive sitting there. Watching $100 accumulate in a car maintenance fund for 8 months while nothing happens feels like money doing nothing. Psychologically it is difficult to not redirect it toward something that feels more immediately useful.

Manual tracking is tedious. Managing multiple sinking funds in a spreadsheet — updating balances, tracking contributions, calculating months remaining — requires discipline that most people do not sustain beyond the first month or two.

All three problems are solvable. The first two with mindset, the third with the right tool.

The Sinking Fund Categories You Actually Need

Not every expense needs a sinking fund. The goal is to capture the predictable large expenses that regularly derail your monthly budget. Here are the categories that matter most:

Essential Sinking Funds — Set These Up First

Car Maintenance and Registration

Cars are predictably expensive. Registration happens annually. Oil changes, tires, brakes, and unexpected repairs happen regularly. Set aside $50-$100 monthly depending on your car’s age and reliability history.

Insurance Premiums

Annual or semi-annual insurance payments — car, home, renters, life — are perfectly predictable. Divide the annual total by 12 and set that aside monthly. When the bill arrives it is already paid.

Medical and Dental

Even with insurance, out-of-pocket medical and dental costs hit most people at least once or twice a year. A modest $30-$50 monthly contribution prevents these from becoming credit card expenses.

Home Maintenance

Homeowners should set aside 1% of their home’s value annually for maintenance and repairs. Renters still face occasional expenses — replacing appliances, minor repairs, moving costs. $50-$100 monthly covers most scenarios.

Lifestyle Sinking Funds — Set These Up Second

Holidays and Gifts

December is financially brutal for people without a holiday sinking fund. Calculate your typical holiday spending — gifts, travel, celebrations — divide by 12, and contribute monthly from January. By December the money is sitting there waiting.

Vacation and Travel

Vacations feel expensive because people pay for them all at once. A dedicated travel sinking fund with a specific target and date makes any vacation genuinely affordable — you are paying for it gradually over months, not scrambling when you book.

Birthdays and Special Occasions

Weddings, milestone birthdays, baby showers, graduations — these appear on the calendar months in advance. A general celebrations fund of $30-$50 monthly handles most of these without derailing your monthly budget.

Strategic Sinking Funds — Set These Up as You Grow

Technology Replacement

Phones, laptops, and tablets have predictable lifespans. If your laptop typically lasts 3 years and a replacement costs $1,200, set aside $33 monthly. When it dies you buy the replacement without touching savings or credit.

Clothing and Wardrobe

Seasonal clothing needs, work attire, children’s clothing — these are predictable annual expenses that most people either overspend on impulsively or underspend on until something wears out at an inconvenient time.

Pet Care

Vet visits, vaccinations, grooming, and unexpected health issues make pet ownership intermittently expensive. A dedicated pet sinking fund of $30-$75 monthly depending on your pet handles routine costs and builds a buffer for unexpected ones.

Education and Professional Development

Courses, certifications, books, conferences — investing in your skills has a reliable return but an irregular payment schedule. A dedicated fund prevents these from feeling like luxuries you cannot afford.

How to Set Up a Sinking Fund Step by Step

Step 1 — List Every Predictable Large Expense

Write down every expense you know is coming in the next 12 months that is not a monthly bill. Include annual, semi-annual, and quarterly expenses. Include irregular but predictable expenses like car maintenance and medical costs based on your history.

Step 2 — Assign a Target Amount and Date to Each

For known fixed expenses — insurance premium, registration — use the exact amount. For variable expenses — car maintenance, medical — use a reasonable estimate based on past spending. Assign a target date — the month you expect to need the money.

Step 3 — Calculate Your Monthly Contribution

Monthly Contribution = Target Amount ÷ Months Until Due DateIf your $1,200 vacation is 8 months away — contribute $150 per month. If your $600 insurance premium is due in 4 months and you are starting now — contribute $150 per month.

Step 4 — Open Separate Tracking for Each Fund

The most important principle in sinking fund management is keeping each fund mentally and practically separate. Mixing them into one “future expenses” savings bucket makes it impossible to know if you are on track for each individual goal.

Step 5 — Automate Contributions as Transactions

Every monthly contribution should be logged as a real transaction — not just a mental note. This keeps your budget accurate, ensures the contribution shows up in your spending tracking, and creates a record of your progress toward each fund.

Step 6 — Review Monthly

Once a month check each fund’s progress — current balance, months remaining, whether your contribution is on track. Adjust contributions when timelines change. Close funds when goals are reached and redirect contributions to new funds.

How Many Sinking Funds Should You Have

There is no universal answer — but a practical range for most people is 4-8 active sinking funds simultaneously.

Fewer than 4 usually means you are still leaving predictable expenses unplanned. More than 10 becomes administratively overwhelming and the monthly contributions per fund become so small they feel pointless.

Start with your 3 highest-priority funds — the expenses that have most frequently derailed your budget in the past. Add funds gradually as your budgeting system matures.

The Psychological Effect Nobody Talks About

Sinking funds do something beyond the practical financial benefit — they fundamentally change your relationship with money.

When every predictable expense has a dedicated fund building toward it, financial anxiety drops dramatically. You stop dreading December. You stop feeling guilty about annual expenses. You stop treating predictable bills as crises.

The money is already there. You planned for it. It arrives and you pay it without stress and without disruption to the rest of your budget.

This is what financial security actually feels like in practice — not a large number in a savings account, but the quiet confidence that comes from knowing every known expense is already covered before it arrives.

Why Manual Sinking Fund Tracking Fails

A spreadsheet sinking fund tracker requires you to manually update balances every month, recalculate months remaining when contributions change, and track contributions separately from your main budget. Most people maintain this for 2-3 months before it becomes too tedious and the funds get neglected.

The version that actually works is one where sinking fund contributions log automatically as transactions, progress bars update in real time, and months remaining recalculate automatically whenever you adjust a contribution amount.

How to Track Sinking Funds Automatically

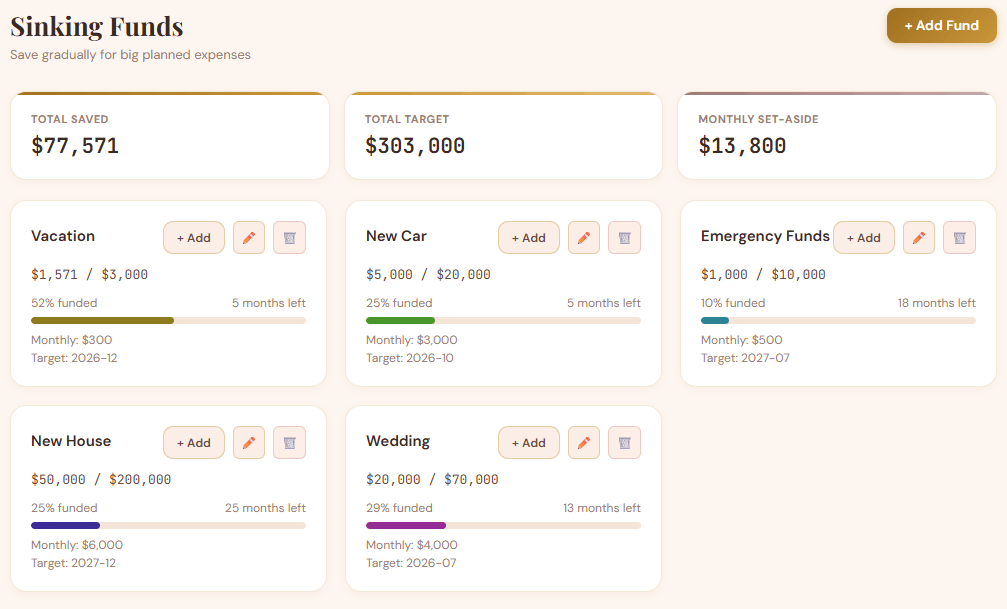

BudgetFlow Pro includes a fully automated sinking fund tracker as part of its complete offline personal finance dashboard. Set a target amount, monthly contribution, and target date for each fund. A visual progress bar shows exactly how many months remain. Every contribution automatically logs as a real transaction keeping your budget accurate.

Eight visual themes, completely offline, one-time purchase, no subscription. Your sinking fund data — like everything else in the dashboard — never leaves your device.

Start tracking your sinking funds here

Frequently Asked Questions About Sinking Funds

Q: Should sinking funds be kept in a separate bank account?

Ideally yes — keeping sinking fund money in a separate high-yield savings account prevents you from accidentally spending it and earns interest while it sits. Some people use one account with mental separation tracked in their budget. Either works as long as the tracking is accurate.

Q: What happens if I need the money before the target date?

Use it — that is what it is there for. Then recalculate your contribution for the remaining months to rebuild the fund before it is needed again. If you consistently need the money early, your monthly contribution may be too low or your target date too far out.

Q: How is a sinking fund different from just saving money?

Regular saving is generally unallocated — money going into savings without a specific purpose or target. A sinking fund is purposeful saving with a specific target amount, specific target date, and specific expense it is designated for. The specificity is what makes it work psychologically and practically.

Q: Can I have a sinking fund for a want rather than a need?

Absolutely — and this is one of the best uses of sinking funds. A vacation sinking fund, a new phone sinking fund, a home renovation sinking fund. Planning for wants the same way you plan for needs eliminates guilt spending and prevents wants from derailing your budget.

Q: What if I cannot afford to contribute to all my sinking funds right now?

Prioritize by consequence. Fund the sinking funds where missing the target would cause the most financial damage first — insurance, car registration, medical. Add lifestyle and strategic funds as your income grows or other expenses decrease.