50/30/20 Rule

Everyone has heard of the 50/30/20 rule. Far fewer people are actually using it correctly.

It sounds simple — split your income three ways and you are done. But the moment you sit down to apply it, questions appear that nobody warned you about. Does my Netflix subscription count as a need or a want? Where does debt repayment go? What if my rent alone takes 60% of my income? What counts as savings versus investing?

These are not edge cases. They are the exact questions that cause most people to either apply the rule incorrectly for months without realizing it, or abandon it entirely after a week of confusion.

This is a complete guide to how the 50/30/20 rule actually works — the real definitions, the common mistakes, how to handle the edge cases, and how to automate the entire calculation so you never have to do it manually again.

Where the 50/30/20 Rule Came From

The 50/30/20 rule was popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book “All Your Worth: The Ultimate Lifetime Money Plan.” The core idea was to give people a simple framework for balancing present spending with future financial security — without requiring a detailed line-item budget that most people abandon within two weeks.

The rule works on after-tax income — meaning the money that actually hits your bank account after all deductions, not your gross salary. This distinction matters more than most people realize and is one of the most common mistakes in applying the rule.

The Three Buckets — Real Definitions

50% — Needs

Needs are expenses you genuinely cannot avoid without serious consequences. The test is simple: if you stopped paying this, would you lose your home, your health, your job, or your legal standing?

Genuine needs include:

- Rent or mortgage payments

- Utilities — electricity, water, gas, internet if required for work

- Groceries — basic food, not dining out

- Health insurance and essential medications

- Minimum debt payments — credit cards, student loans, car loans

- Transportation to work — car payment, fuel, public transit

- Childcare if required for you to work

What most people wrongly put in Needs:

- Streaming subscriptions — Netflix, Spotify, Disney Plus

- Gym memberships

- Phone upgrades

- Dining out

- Amazon Prime

- Coffee subscriptions

These feel essential because you use them daily. They are not needs. They are wants you are very attached to — which is completely fine, but they belong in the 30% bucket not the 50% bucket.

30% — Wants

Wants are everything that improves your life but is not strictly necessary for survival or employment. This is the category most people either dramatically overspend in without realizing, or feel guilty about entirely.

The 50/30/20 rule is not about eliminating wants. It is about consciously deciding how much of your income goes toward them.

Genuine wants include:

- Dining out and takeaway

- Streaming services — Netflix, Spotify, YouTube Premium

- Gym membership

- Hobbies and entertainment

- Shopping — clothing beyond basics, home decor, gadgets

- Vacations and travel

- Subscriptions — news, apps, software

- Upgraded phone beyond what you need for work

The 30% allocation is genuinely generous. On a $4,000 monthly take-home income, 30% is $1,200 for wants. Most people who think they cannot afford to save discover after tracking their wants spending that they are spending $1,500-$1,800 in this category — which is where the deficit is coming from.

20% — Savings

The savings bucket is the most misunderstood of the three — because “savings” in the 50/30/20 framework means something broader than just a savings account.

The 20% savings bucket includes:

- Emergency fund contributions

- Retirement contributions — 401(k), Roth IRA, pension

- Investment contributions — stocks, ETFs, index funds

- Extra debt payments beyond minimums — this is critical

- Sinking funds — saving for future planned expenses

- General savings account contributions

The reason extra debt payments belong in savings rather than needs is philosophical but important. Your minimum payment is a need — it prevents default. Any payment above the minimum is a financial decision that accelerates your path to wealth — which is savings behavior, not necessity.

The Most Common 50/30/20 Mistakes

Mistake 1 — Using Gross Income Instead of Net

If your salary is $60,000 but your take-home after tax and deductions is $44,000, your 50/30/20 calculation runs on $44,000 — not $60,000. Using gross income inflates every bucket and makes your savings target look smaller than it actually should be.

Mistake 2 — Putting Debt Minimums in Savings

Minimum debt payments are a need — not savings. Missing them damages your credit score and incurs penalties. They belong in the 50% needs bucket. Only extra payments above the minimum belong in the 20% savings bucket.

Mistake 3 — Treating the Rule as a Perfect Split

The 50/30/20 rule is a guideline not a law. If you live in an expensive city where rent genuinely takes 40% of your income, your personal version might be 60/20/20 or 55/20/25. The framework matters more than the exact percentages. The goal is awareness and intentionality — not perfect adherence to three numbers.

Mistake 4 — Calculating It Once and Never Revisiting

Your income changes. Your expenses change. A raise, a new subscription, a rent increase, a paid-off debt — all of these shift your percentages. The 50/30/20 rule only works if you recalculate it every single month against your actual income and actual spending.

This is where most people fail — not in the initial setup, but in the monthly maintenance.

How to Actually Calculate Your 50/30/20 Split

Step 1 — Find Your Monthly After-Tax Income

Add up everything that hits your bank account monthly — salary, freelance income, side income, rental income. Use actual deposits not gross figures.

Step 2 — Calculate Your Three Targets

- Needs target: Monthly income × 0.50

- Wants target: Monthly income × 0.30

- Savings target: Monthly income × 0.20

Step 3 — Categorize Every Expense

Go through last month’s transactions and assign every expense to Needs, Wants, or Savings. Be honest — this step is where most people discover uncomfortable truths about their spending.

Step 4 — Compare Actual vs Target

How does your actual spending in each bucket compare to your target? Most people discover they are over in Wants and under in Savings — often significantly.

Step 5 — Adjust and Track Monthly

Identify one or two wants you can reduce this month. Redirect that difference to savings. Recalculate next month with actual numbers.

Why Manual Calculation Fails After Month Two

The 50/30/20 rule works brilliantly in theory. In practice, manually categorizing every transaction every month is tedious enough that most people stop doing it.

The calculation itself is not difficult. The data collection is. Going through bank statements, categorizing each transaction, adding up totals by category, comparing to your income targets — this takes 1-2 hours monthly if done manually. Most people do it once, feel good about it, and never do it again.

The only version of the 50/30/20 rule that produces long-term financial results is one that runs automatically — where categorization happens as you log transactions and the split calculates itself without you touching a spreadsheet.

How to Automate Your 50/30/20 Budget

The most practical way to automate the 50/30/20 rule without a subscription app is a finance dashboard that handles the calculation for you.

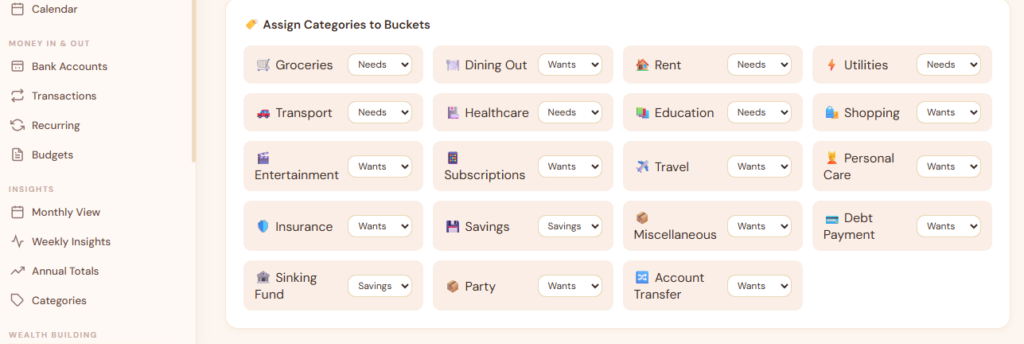

Assign each spending category to its bucket once — groceries go to Needs, Netflix goes to Wants, investment contributions go to Savings. After that single setup step, every transaction you log is automatically counted toward the right bucket and your 50/30/20 split updates in real time.

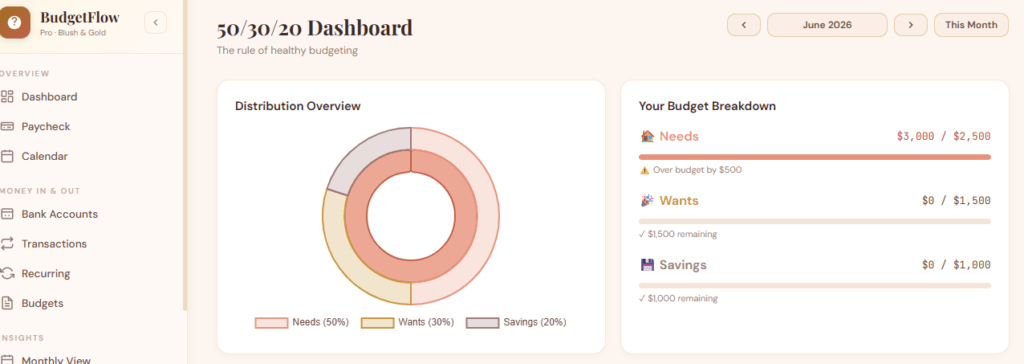

At the end of every month you see exactly where you landed — did you hit 50/30/20 or did you end up at 55/35/10? Browse any past month to see your historical split. Identify patterns across 6 months of data. Watch your savings percentage grow over time as your financial habits improve.

This is what a proper 50/30/20 budget rule app does — not a calculator you run once, but an automated dashboard that tracks your split continuously across every transaction you log.

BudgetFlow Pro includes a fully automated 50/30/20 dashboard that does exactly this — assign categories once, get your split calculated automatically every month, browse any historical month instantly. Eight visual themes, completely offline, one-time purchase, no subscription.

enigmaeasel.com/product/all-in-one-budget-planner-web-app

What Your 50/30/20 Numbers Actually Tell You

Once you have one month of real data, three things become immediately clear:

If Needs exceeds 50%: Your fixed costs are too high relative to your income. The solution is either increasing income or reducing fixed costs — moving to a cheaper home, refinancing debt, cutting insurance costs. Reducing wants spending alone will not fix a needs problem.

If Wants exceeds 30%: This is the most common situation and the most actionable. Identify your top 3 wants by spending amount. Reducing each by 20% is usually painless and redirects significant money to savings.

If Savings is below 20%: This is a symptom, not a cause. Fix whichever of the above two categories is over budget and savings corrects itself automatically — because your income is fixed, every dollar you remove from one bucket goes to another.

The 50/30/20 Rule for Different Income Levels

Lower Income — Under $3,000/month Take-Home

The 50% needs target is extremely difficult at this income level in most cities. Rent alone often exceeds 40%. The framework still applies but the percentages shift — aim for 60/20/20 and focus entirely on gradually increasing income to make the standard 50/30/20 achievable.

Middle Income — $3,000-$7,000/month Take-Home

This is the sweet spot where the 50/30/20 rule works exactly as designed. Needs should be manageable at 50%, there is real money in the wants bucket to enjoy life, and 20% savings builds wealth meaningfully over time.

Higher Income — Above $7,000/month Take-Home

At higher incomes the 30% wants bucket becomes very generous. Consider shifting to a 50/20/30 model — keeping needs at 50%, reducing wants to 20%, and pushing savings to 30%. The compound effect of 30% savings at higher income levels accelerates wealth building dramatically.

Frequently Asked Questions About the 50/30/20 Rule

Q: Does the 50/30/20 rule work if my income varies month to month?

Yes — use your lowest typical monthly income as your baseline for calculating targets. In higher income months direct the extra entirely to savings. This creates a conservative baseline that protects you in lower months while accelerating savings in higher ones.

Q: Where does my emergency fund go — needs or savings?

Emergency fund contributions go in the 20% savings bucket. Once your emergency fund is fully funded — typically 3-6 months of expenses — redirect those contributions to investments or extra debt payments within the same savings bucket.

Q: Should I follow 50/30/20 or pay off debt first?

Both simultaneously. Minimum debt payments belong in your 50% needs bucket. Extra debt payments belong in your 20% savings bucket. The 50/30/20 framework accommodates aggressive debt payoff — simply allocate more of your 20% savings to extra debt payments until debts are cleared, then redirect to investments.

Q: What if I cannot hit 20% savings right now?

Start wherever you are. If you can only save 5% right now, save 5% consistently and increase by 1-2% every three months. The habit of saving matters more than the percentage in the early stages. The 20% target is a destination, not a requirement for starting.

Q: Is the 50/30/20 rule better than zero-based budgeting?

They solve different problems. Zero-based budgeting gives you granular control over every dollar — better for people with spending problems or aggressive financial goals. The 50/30/20 rule gives you a simple framework that requires less maintenance — better for people who want financial awareness without obsessive tracking. Many people start with 50/30/20 and move to zero-based budgeting once they want more control.

Final Thought

The 50/30/20 rule is not magic. It is a framework for making intentional decisions about three things — what you need, what you enjoy, and what you are building toward.

Most people who fail at it do not fail because the rule is wrong. They fail because they calculate it once, feel organized for a week, and never look at the numbers again.

The version that actually changes your financial situation is the one you run every single month, automatically, against real transaction data — not the one you calculate manually on a Saturday afternoon and forget about by Wednesday.

That consistency is what separates people who talk about the 50/30/20 rule from people whose savings account actually reflects it.